1. Questions

To assess the possible future effects of climate policies on power systems, decision makers often rely on generation expansion models (Bistline et al. 2023). Such models estimate the optimal set of investment and operating decisions of power market participants. While state-of-the-art models are technologically rich, they often greatly simplify the role of risk in power systems.

Policy analyses commonly assume the existence of idealized markets that allow investors to insure themselves against any possible future. However, real markets fail to provide for such complete risk hedging (Radner 1970). In power systems, this is illustrated by the limited liquidity of long-term markets (Batlle et al. 2023), which is known as the missing market problem (Newbery 2016). As a result, investors face considerable risk, which can cause under-investment. We consider the implications of this phenomenon for government efforts to incentivize clean energy investments.

Specifically, we ask: how are the effectiveness and cost of popular climate policies affected by the missing market problem? Our focus is on Investment Tax Credits (ITCs), such as those in the U.S. Inflation Reduction Act, and CO taxes.

2. Methods

We model a power system with risk-averse investors and risk-averse consumers participating in a perfectly competitive, energy-only market. To assess the impact of the missing market problem, we compare two cases. First, in a benchmark, “complete markets” case, investors and consumers share risk by trading long-term contracts. This is represented, as in prior work, by modeling the electricity market as the cost-minimization problem of a risk-averse central planner (Dimanchev et al. 2023). Second, in our main, “missing markets” case, investors and consumers do not trade long-term contracts. To model this, we use the equilibrium model developed by Dimanchev et al. (2023). This model disaggregates investor and consumer decision-making, precluding risk sharing (i.e., long-term contracts) between market participants. In all other respects, the model is equivalent to the complete market benchmark. Sensitivity analyses further compare our modeling to more traditional models that assume risk-neutral agents or that omit uncertainty entirely (supplementary document Section S3).

In our illustrative experiments, risk-averse investors optimally deploy gas plants, wind, solar, and Li-ion batteries. These resources are operated in a least-cost way by a system operator at an hourly resolution in different scenarios for 2050. Meteorological variability is captured in detail using 16 representative weeks based on data for the New England power system (Dimanchev et al. 2023). Investments are made under uncertainty in overall demand, which captures uncertainty in electrification and hydrogen electrolysis. This is represented with four equi-probable scenarios, where demand in each hour is shifted by -25%, -12.5%, +12.5% and +25% relative to projected demand. Risk aversion is modeled using the commonly employed Conditional Value-at-Risk (CVaR). The model’s formulation is shown in the supplementary document (Section S1).

We measure policy effectiveness as a reduction in power system emissions resulting from a given policy. Policy cost is defined as an increase in risk-adjusted system cost. We use risk-adjusted system cost to represent the perspective of a government that considers the risk preferences of market participants (and therefore risk-adjusts its measure of total costs), as recommended for benefit-cost analyses (OMB 2023). In our context, this is equivalent to the perspective of a government aiming to maximize social welfare, reflective of private risk preferences. The supplementary document provides the mathematical formulation used for calculating the risk-adjusted system cost (Section S2.2) and a sensitivity test using risk-neutral system costs (S4), where our main findings continue to hold.

3. Findings

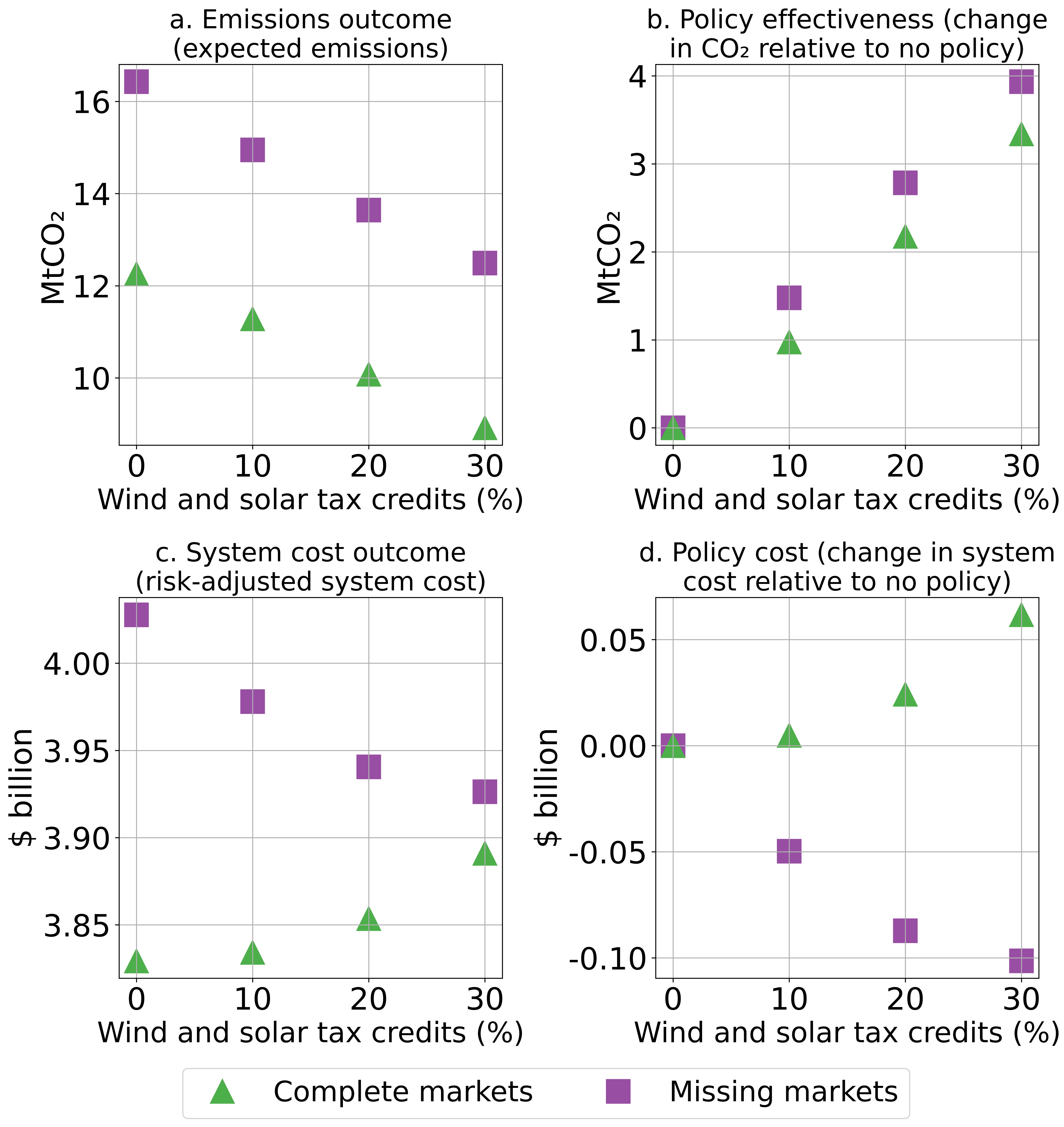

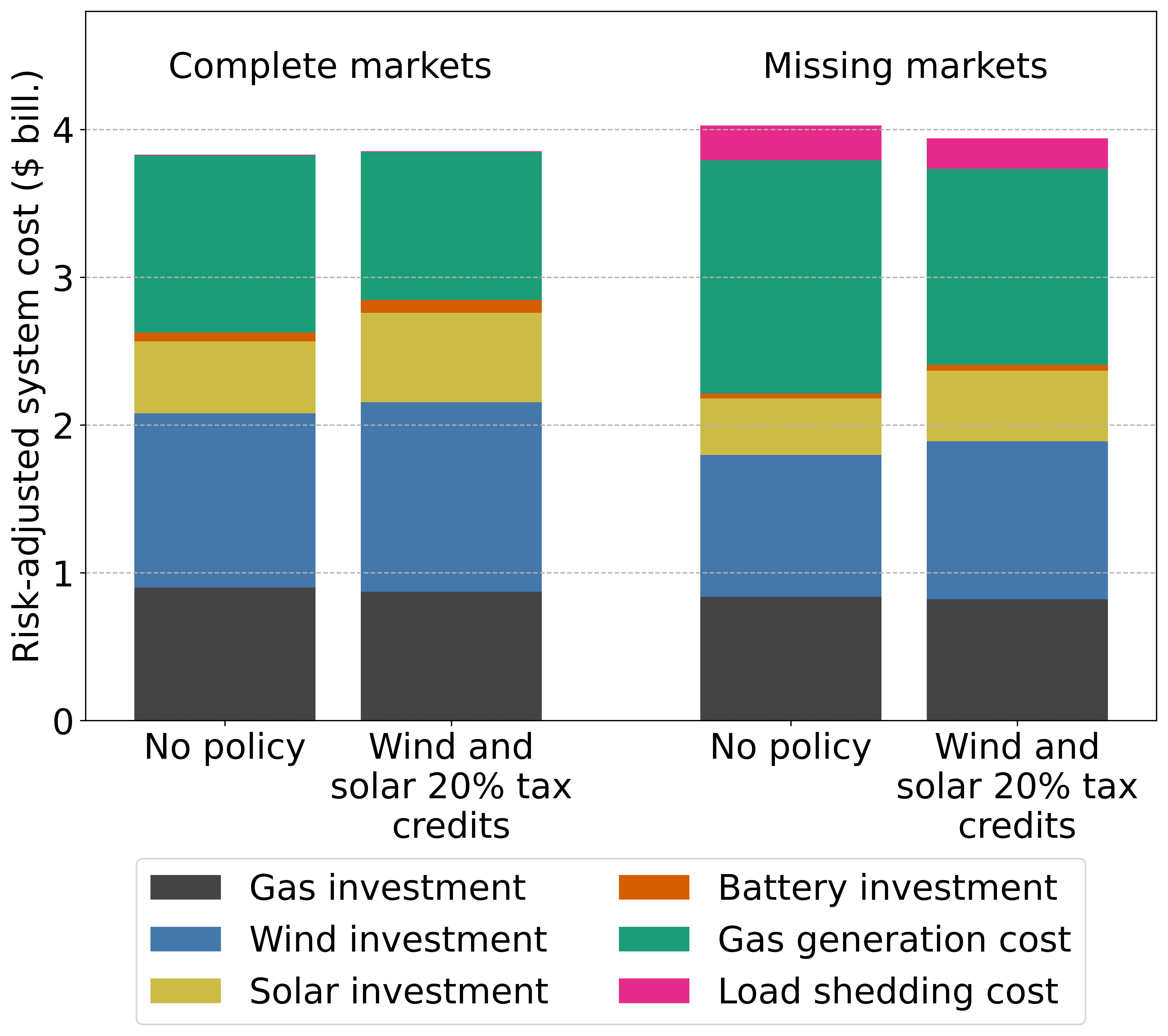

Power system outcomes with different ITCs are displayed in Figure 1-a/c. Expected emissions are generally higher in the case of missing markets (Figure 1-a). This is because the missing market problem skews investments away from wind and solar in our experiments, as discussed in Dimanchev et al. (2023) and illustrated in Figure 2. This result suggests that renewable investment is sub-optimally low in economies with missing risk markets. Under-investment in renewables and other technologies results in higher risk-adjusted system costs, in part by leading to unserved demand, when risk markets are missing relative to a case of complete markets (Figure 1-c, and Figure 2).

We find that the costs of ITCs are lower when long-term markets are missing than when markets are complete (Figure 1-d). This is because ITC policy has two counterveiling effects in the missing markets case. First, as expected, ITCs impose a cost by distorting the market equilibrium. Second, ITCs provide an economic benefit by counteracting inefficiencies caused by the missing market problem. The existence of this second effect is an example of the well-established potential for government interventions to provide economic benefits when the economy is in a second-best equilibrium (Lipsey and Lancaster 1956), a classic case being the revenue recycling effect of environmental taxes amid pre-existing tax distortions (Goulder et al. 1999). Since the missing market problem distorts investments away from wind and solar, its effects are partly corrected by ITCs, which encourage investment in these technologies (Figure 2). The additional investments reduce operating costs, especially in the highest-demand scenario, which is of particular importance to risk-averse consumers. Remarkably, we estimate ITC costs to be negative (Figure 1-d). This indicates that the second of the two effects discussed above outweighs the first (sensitivity tests are provided in the supplementary document sections S4-5).

We also observe that policy effectiveness is higher in the case of missing markets relative to complete markets (Figure 1-b). This can be explained by the fact that emissions in the latter case are lower to begin with, making additional reductions more difficult. In combination with our cost estimates, this result shows that policy efficiency is higher with missing markets (i.e., average cost per ton CO abated is lower).

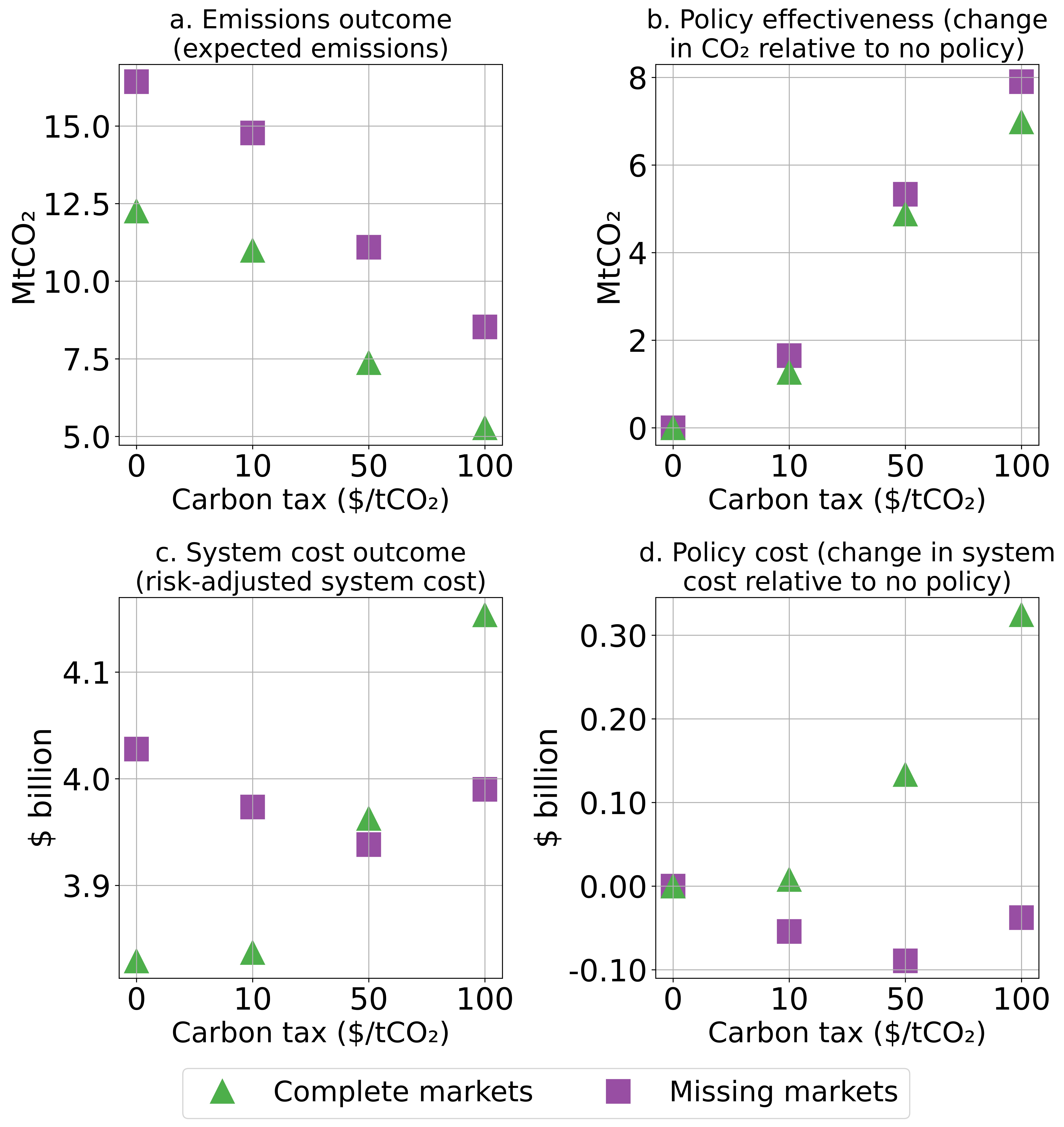

A CO tax also corrects missing market inefficiencies, making its economic cost lower when long-term markets are missing (Figure 3-d). By raising the variable cost of the price-setting gas plant, the tax increases renewable revenues, encouraging greater (and more efficient) levels of renewable investment. Our illustrative experiments also show CO tax costs to be negative in the presence of missing markets (see supplementary document sections S4-5 for sensitivity tests). The CO tax reduces more emissions under missing markets (Figure 3-b). This further implies that CO taxes cost less per ton CO abated when risk markets are missing.

_at_a_lowe.jpg)

We expect the real-world effects of the missing market problem to be smaller than what we observe, as economies generally feature some risk trading, though incomplete. This and other assumptions, such as our limited technological options and lack of demand-side flexibility, make our results merely illustrative. Nevertheless our findings suggest a need for further consideration of the missing market problem in climate policy analyses.

Acknowledgements

We thank three anonymous reviewers for helpful feedback. This research was funded by CINELDI, an 8 year research center part of the Norwegian Centers for Environment-friendly Energy Research (FME) (grant number: 257626).