1. Questions

The COVID-19 pandemic severely disrupted supply chains around the world (Pujawan and Bah 2022). Many consumers in the United States experienced important shortages of goods and companies struggled with important delays on the procurement side of their business. As a consequence of this disruption, governments and private companies had to pivot towards more resilient strategies that could increase their preparedness for similar events in the future (Moosavi, Fathollahi-Fard, and Dulebenets 2022). One of the solutions preconized by US companies that are supplied in manufactured goods was to diversify their manufacturing base by shifting some of their operations from China to Mexico (van Hassel et al. 2022). This shift is commonly referred to as “nearshoring”, or the delocalization of operations to a location nearer to the US (Hartman et al. 2017).

The supply chain pivot from China to Mexico - the US’ 3rd and 2nd largest trading partners - through nearshoring strategies has been discussed in existing literature (Bravo 2022; Pérez Hincapié 2022; van Hassel et al. 2022; Jayashankar and Torres 2023; Pietrobelli and Seri 2023) and justified in part because of shorter supply chain delays, a more educated workforce and cultural proximity to the US. Chinese firms themselves have setting up plants in Mexico to better supply US firms (Goodman 2023). While Torres (2023) does find a general nearshoring effect using empirical data, no study to date using historical trade data grouped by commodity classification has yet been undertaken, between the United States, China and Mexico. Thus, we ask: did exports from China to the US shift to Mexico after the COVID-19 pandemic? Further, in which sectors was this shift most palpable? The novelty of this study comes from the use of data grouped by industrial sector, to understand how US firms from some sectors changed their procurement strategies after the pandemic.

2. Methods

Data used for this study comes from the United States Census Bureau (United States Census Bureau 2023), which offers comprehensive sector- and country-specific trade data pertaining to goods exports to the US. We compile monthly data from January 2019 to March 2023, from roughly one year before the start of the COVID-19 pandemic. To analyze the data, we employ a comparative time series design by comparing export volumes (in USD) to the US from China to those from Mexico and by plotting them over time. We underline historical trends in our diagrams by using polynomial trendlines in the third degree. We do this for total export volumes and for each of the sector-based tallies across 15 categories based on the Harmonized System (HS) codes used by the United States Census Bureau. The goods categories and their respective HS codes are shown in Table 1. More information about specific HS codes can be obtained on the website of the United States Census Bureau (United States Census Bureau 2023).

3. Findings

Tables 2 and 3 show the export volumes by sector to the US from China and Mexico respectively. There are important differences in the export volumes for each sector and by country. China mainly exports machinery and electrical equipment, various manufactured goods and processed materials (plastics, rubbers, metals, chemicals) to the US. Mexico also exports machinery and electrical equipment, various manufactured goods and processed materials agrobusiness-related products, but also a lot of transportation equipment (cars) or agrobusiness-related products (foodstuffs, vegetables, animal products).

We see that there are steady export volumes from China and Mexico to the US throughout 2019. COVID-19 cases first appear in China during Q1 of 2020 (World Health Organization 2023), disrupting their supply chains and reducing their export volumes the US. In Mexico, we see the effect of the pandemic on the supply chain during Q2 because the virus makes landfall in the country later in the year (Ibarra-Nava et al. 2020). By Q3, export volumes to the US are back to pre-pandemic levels for both countries. This could indicate that US firms benefitted from resilient supply chains in China and Mexico in the immediate aftermath of the initial disruption.

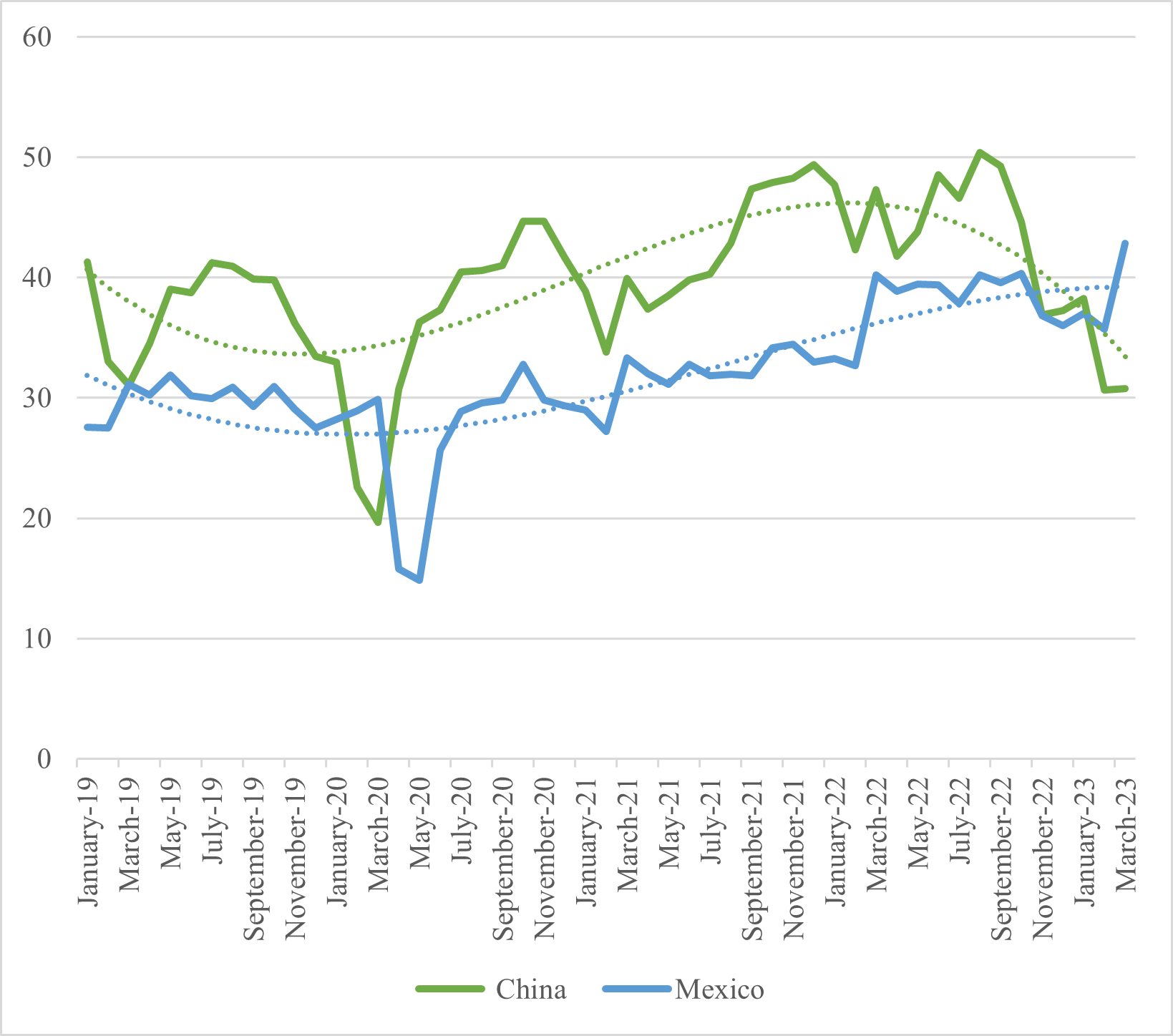

Figure 1 plots the total export volumes from both countries and related trendlines. In the 18 months following the disruption in Q1 and Q2 of 2020, supply chains of both countries to the US outperform pre-pandemic exports. However, the start of 2022 marks a change in trend between China and Mexico. China’s export volumes start to fall dramatically, whereas Mexico’s continue to increase steadily, continuing to outperform pre-pandemic exports. By the end of our study period, March 2023, there are more exports from Mexico to the US than from China. This confirms in part the hypothesis formulated in the literature that part of US firms’ supply chains were displaced to Mexico.

.png)

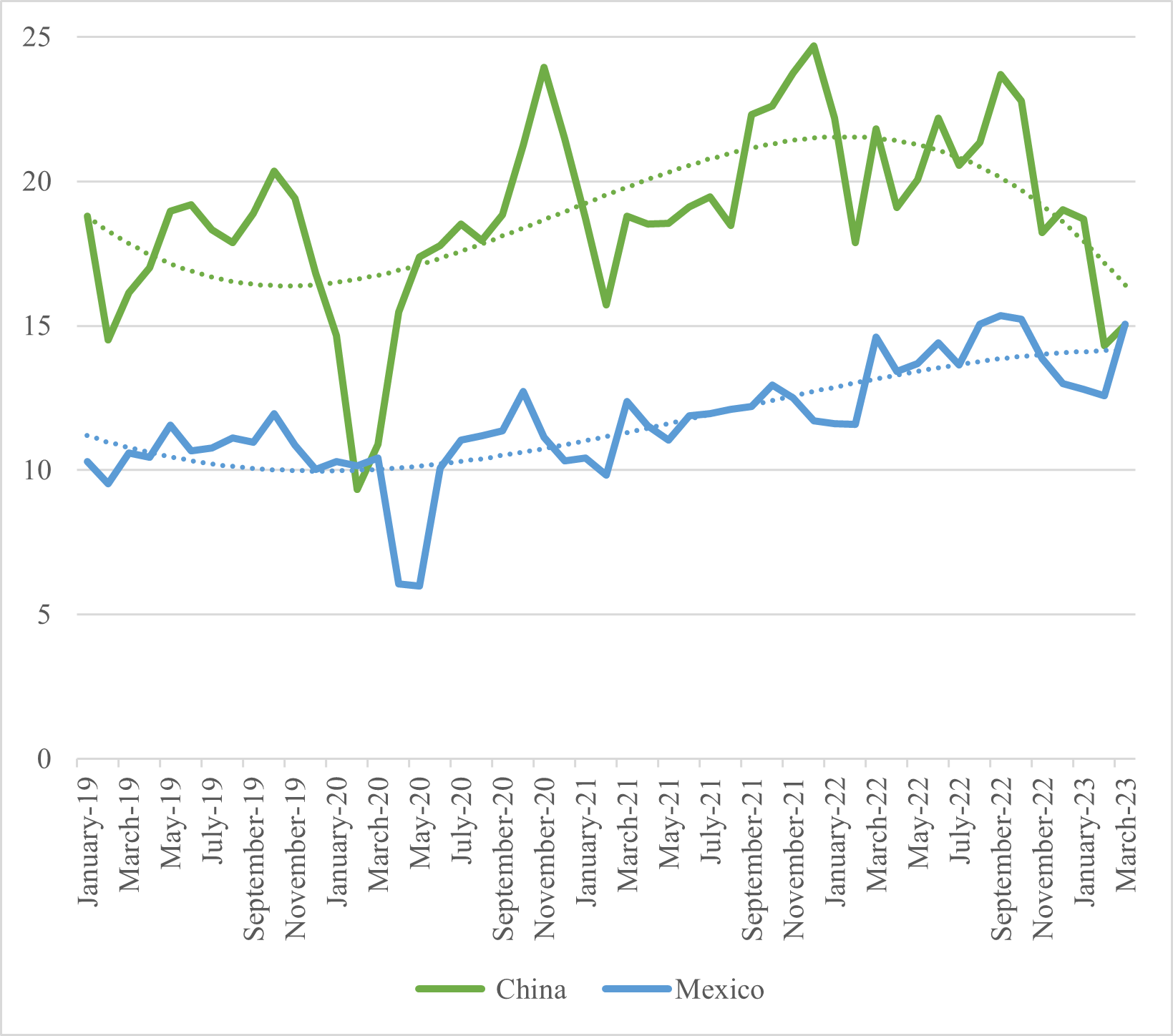

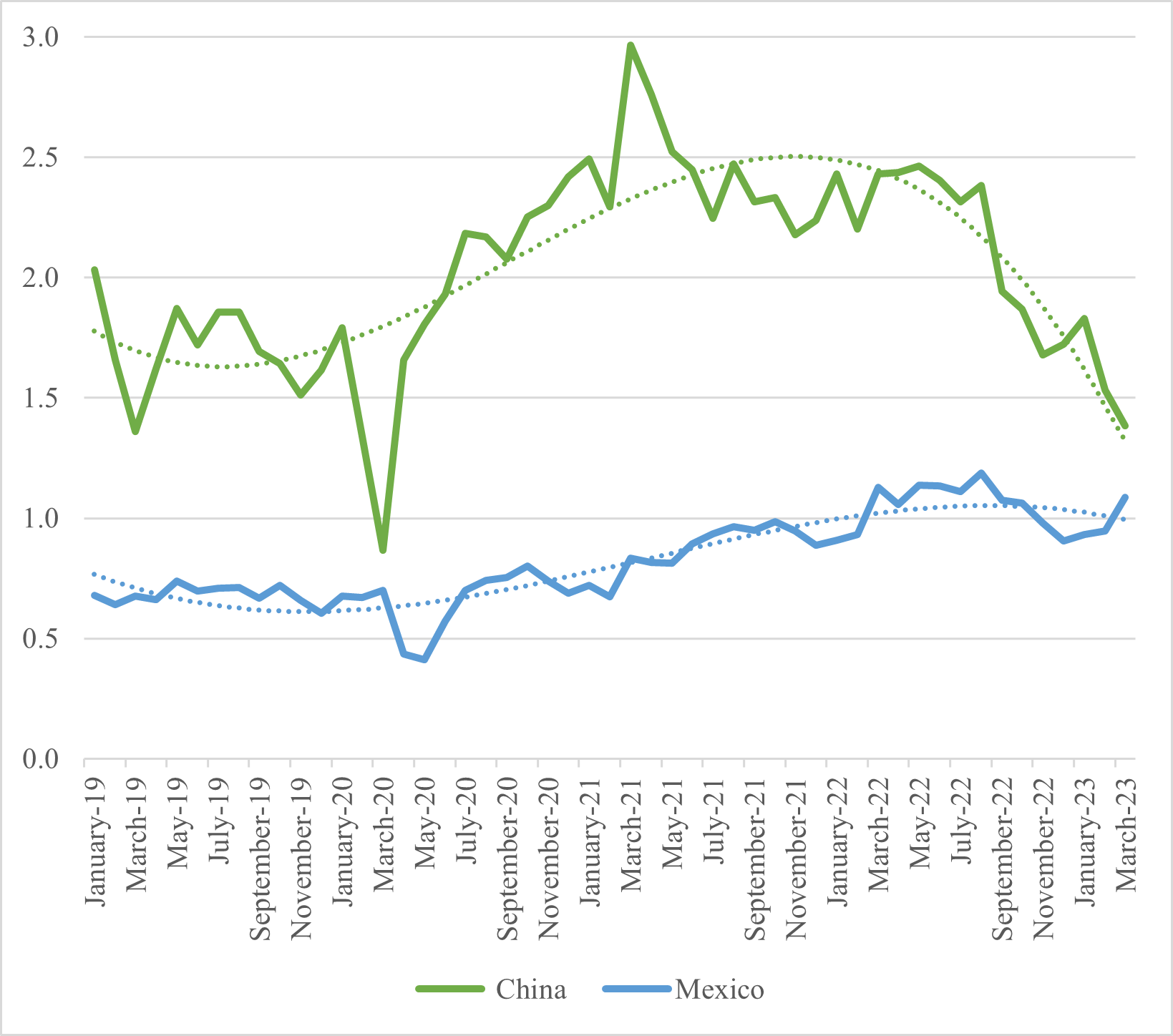

Figures 2 and 3 plot two sectoral categories in our study to better illustrate the point made above. Figure 2 shows the trends for exports in machinery and electrical components, exhibiting the same behaviour as total export volumes. This category includes components for the automotive, aeronautics and electronics industries, all time-sensitive sectors with complex supply chains where reduced uncertainty is an advantage. These industrial sectors also represent an important part of Mexico’s economic output. Even for categories that have less complex supply chains, the same trend is palpable. This is notable for plastics and rubbers, shown in Figure 3, where China’s exports to the US shows a very important downward trend by 2023.

.png)

.png)

Our findings show that both China and Mexico were able to quickly recover from the disruption of their supply chains by the COVID-19 pandemic. However, only Mexico was able to improve its performance in supplying the US post-recovery. On the other hand, China seems to be progressively losing ground on its share of supplying the US market with goods. This suggests that US firms have indeed pivoted part of their supply chains from China towards Mexico in the aftermath of the disruption caused by COVID-19, to benefit from a more resilient procurement strategy. This could be because of two things. First, that the supply chain delays related to procurement from China no longer answer the US’ needs. Second, that some of the advantages of Mexican procurement, i.e., shorter supply chain delays, a more educated workforce and cultural proximity to the US, are strategic advantages. For example, the automotive industry, where Mexico is an intermediate step and receives components to be assembled in a car that is then shipped to the US (Torres 2023), is a good example of how proximity can be doubly beneficial. Our research tracks this shift in strategy and offers researchers and policymakers empirical evidence of how trade between China, Mexico and the US changed during the most important event of supply chain disruption in recent history. We can conclude that regional proximity has a non-negligible impact on long-term supply chain resilience.

ACKNOWLEDGMENTS

We thank Rafael Batres for his insights on the Mexican economy.