1. Questions

Forecasts for anticipated curtailed energy conclude that energy storage systems (ESSs) must be more responsive to irregular energy sources (Zakeri and Syri 2015) and thus, long-term energy storage has gained substantial research funding (energy.gov 2022; gov.uk 2022). Previous studies have contributed to understanding the functional limitations, technical characteristics, and optimal strategies for modelling ESSs (Cutter et al. 2014; Díaz-González, Sumper, and Gomis-Bellmunt 2016; Dunn, Kamath, and Tarascon 2011; Evans, Strezov, and Evans 2012; Karellas and Tzouganatos 2014; Punys et al. 2013). These parameters documented in literature have been used within the model. However, further research is required to explore ESS that can generate revenues from interacting with the electric grid or, in the case of hydrogen, participation in both electric and hydrogen markets.

Here, the following questions are addressed: 1) What are the financial requirements for energy storage in resilient energy systems? and 2) How do different operational modes and market participation influence the overall financial implications for ESSs?

2. Methods

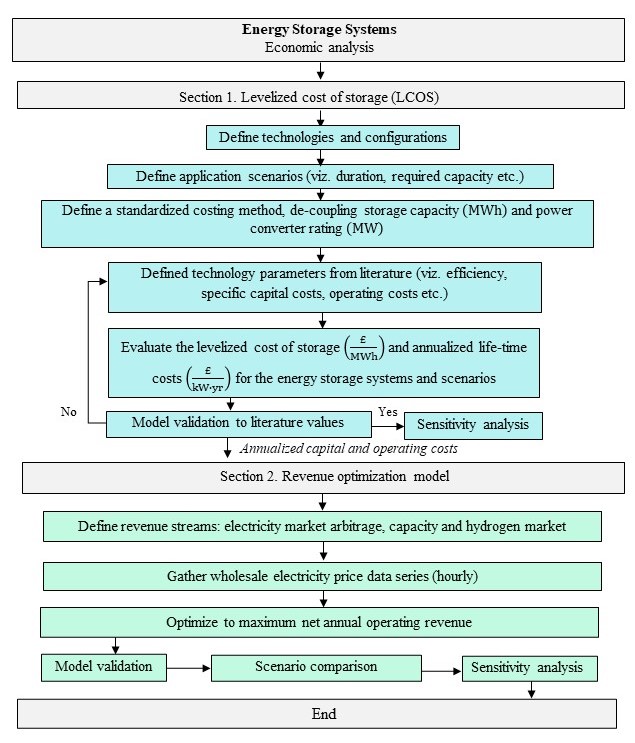

In order to directly compare ESSs, a standardized economic assessment framework has been established to evaluate the respective annualized life-cycles costs (LCCs) and annual revenues, shown in Figure 1. It includes fixed costs (£/kW/year), variable costs (£/MWh), and accommodates revenue stacking options. An economic assessment of ESSs includes the technology itself (i.e. round-trip efficiency, capital costs- fixed and variable, and replacement costs) and exogenous factors related to the final ESS application (i.e. electricity price, energy demand, and project time horizon) (Moseley and Garche 2014). Therefore, parameters characterizing both the storage technology and storage application have been considered (National Grid ESO 2021).

The Supporting Information elaborates on the equations used for the LCC model, the profitability analysis, and an assessment of model metrics. The Supporting Information also includes the literature used for costing and technology performance. Briefly, an ESS’s LCC represents the cost per given power output in an annualized form over the ESS’s lifespan. The model presented here builds upon and is validated by other literature sources (Díaz-González, Sumper, and Gomis-Bellmunt 2016; Moseley and Garche 2014). The objective function of the profitability analysis is to maximize net annual operating profit from charging and discharging sequences, given perfect foresight of hourly UK 2019 wholesale electricity prices (NordPool 2020). This model calculates profit based on storage capacity, charge level and ensures that charging and discharging are de-coupled and cannot happen simultaneously. Due to wholesale foresight, the model allows for ESSs to be able to optimise between selling electricity or hydrogen upon primary energy production and storing energy to be sold at a more profitable energy price. The cost of purchasing electricity and natural gas, such as in some compressed air energy storage (CAES) systems, are included in the variable costs. Storing curtailed renewable energy will be important for future energy system, specifically large storage systems, as these periods offer negative energy pricing. This is especially advantageous for storage systems with high variable costs.

3. Findings

What is the levelized cost of potential future energy storage systems?

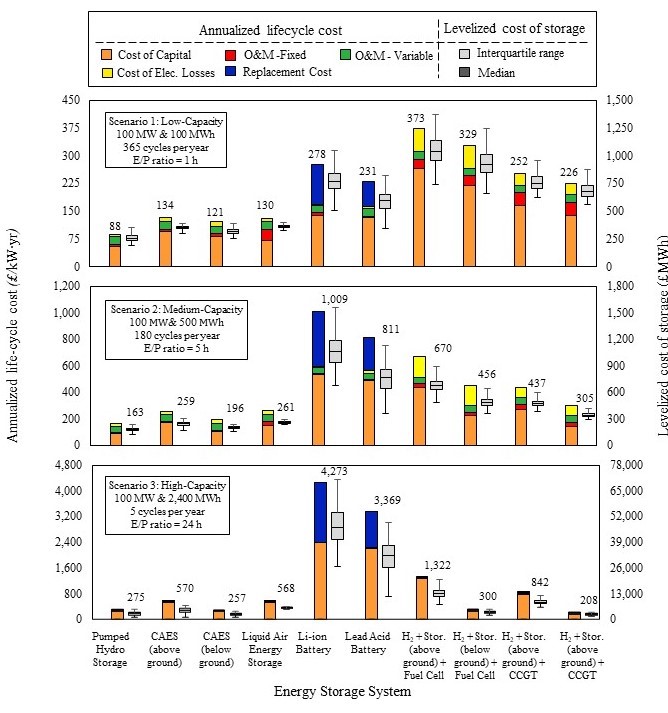

Three capacity scenarios are used to highlight trends in opting for larger storage applications with longer discharge times for all ESS in Figure 2. For the low-capacity scenario (Fig. 2 top), pumped hydro storage results in the most economical ESS (£88/kW/year), followed by CAES with underground storage (£121/kW/year) and liquid air energy storage (£130/kW/year). The cost of capital contributes to the majority of the LCC for all systems and includes replacing batteries over the 30-year analysis period. In Scenario 1, hydrogen systems can be seen to have relatively high capital costs and their low round-trip efficiencies result in higher operating costs for scenarios with increased cycling.

_and_levelized_cost_of_electricity_(right-axis)_for_.jpg)

The cost of hydrogen ESS capital dominates the LCC due to the high-power converter costs. Therefore, with lower cycling, the levelized cost of storage (LCOS) for hydrogen storage decreases. Additionally, as the capacity for hydrogen ESS increases, underground hydrogen storage LCOS decreases significantly compared to above ground storage.

The LCOS stochastic analysis (Fig. 2 grey bars) show that all systems, except battery systems, produce a lower LCOS with higher storage capacity systems despite capital costs increasing. This is due to less frequent cycling in the Medium-Capacity scenario but greater overall load hours offsetting the increase in the cost of capital.

These results conclude that low cycling and high-capacity results in the lowest cost of hydrogen storage, whereas pumped hydro, CAES, or liquid air offer the lowest LCOS in a range of cycling and capacity scenarios, which is necessary for resilient ESSs.

What is the operating profit potential for hydrogen energy storage systems in wholesale markets?

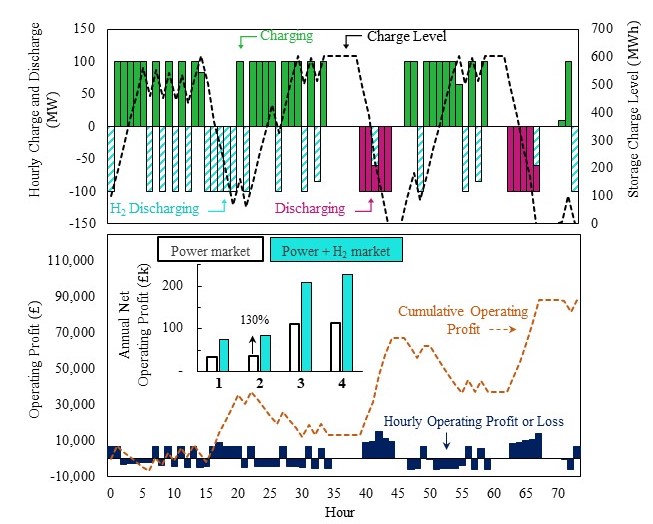

Fig. 3 shows the dispatch profile of the hydrogen and CCGT system with underground storage, illustrating how the model incorporates wholesale electricity prices (Fig. 3 top) when provided with foresight to UK wholesale electricity prices. It allows for maximizing profitability by dictating charging and discharging events (Fig. 3 middle) over 72 hours. Hydrogen systems are also given the option to discharge hydrogen (Fig. 3 middle) at a price of £50/MWh, in-line with levelized hydrogen production estimates from steam methane reforming (SMR) (International Energy Agency 2019). The accompanying cumulative profit plot (Fig. 3 bottom) shows the hourly profit or loss as bars, which the model seeks to maximize at the end of the specified time length.

_used_for_validation_of_hourly_charge_and_discharg.jpg)

The inset in Fig. 3 (bottom) shows hydrogen-based storage systems to contribute to hydrogen energy systems in the optimization model (blue bars), compared against revenues solely operating in electricity markets (white bars). All stored electricity is also fully discharged at the end of the specific time length to ensure that the model maximizes the total operating revenue rather than solely storage revenue.

Hydrogen systems increase their profitability when selling electrolyzed hydrogen into the hydrogen market, avoiding the efficiency loss of converting the stored hydrogen back into electricity. Fig 3 (middle) shows the difference in participation of stored hydrogen in either electricity markets (pink bars) or in hydrogen markets (blue hatched). The model opts to participate in the hydrogen market at a much higher frequency than the electric energy market due to the high cost of energy conversion of hydrogen to electricity. Only with high wholesale electricity cost (Fig. 3 top) will there be a profit of selling stored hydrogen back to an electric market.

The fuel-cell systems (categories 1 and 2 in Fig. 3 bottom insert) had a 120% increase in revenue for the above-ground storage system, and a 130% increase for the below-ground storage system when participating in the hydrogen markets. This limits the profitability potential of stored hydrogen, the energy markets it can participate in, and the overall ability to contribute to a resilient energy market. This concludes that the profitability potential of hydrogen storage systems, even with revenue stacking, is limited to restricted or niche hydrogen markets. The potential for operating hydrogen energy storage systems profitably is low.

Acknowledgements

The authors would like to acknowledge the Centre for Sustainable Road Freight 2018-2023 (EP/R035199/1) for funding this research.