1. QUESTIONS

Switzerland aims at reaching net zero CO2 emissions by 2050, but progress in the entire food sector has been limited to date—including in the dairy processing industry, despite the absence of (difficult to abate) methane emissions and comparatively low process temperatures. Because many think the supply of cheap gas has come to an end in Europe (cf. Figure 31 in BloombergNEF’s proprietary report on the German power market (2022), the section on natural gas in chapter 2.4.2 of IEA’s World Energy Outlook (2022), and the supplemental information of this article), here we ask whether it is economically feasible for producers of dairy products in Switzerland to switch to low-carbon alternatives, given the current energy and climate policy landscape in the country.

2. METHODS

A techno-economic model was implemented to compare the costs of four heating technologies relevant for the Swiss dairy sector (cf. Figure 1): gas boilers, biomass boilers, electric boilers, and electric heat pumps. Other technological decarbonization options as, e.g., synthetic fuels, carbon capture and advanced electricity-based options (e.g., reverse osmosis) were not considered. Hybrid systems were neither considered for the sake of simplicity. Also, theoretically conceivable co-benefits from cooling were neglected for heat pumps.

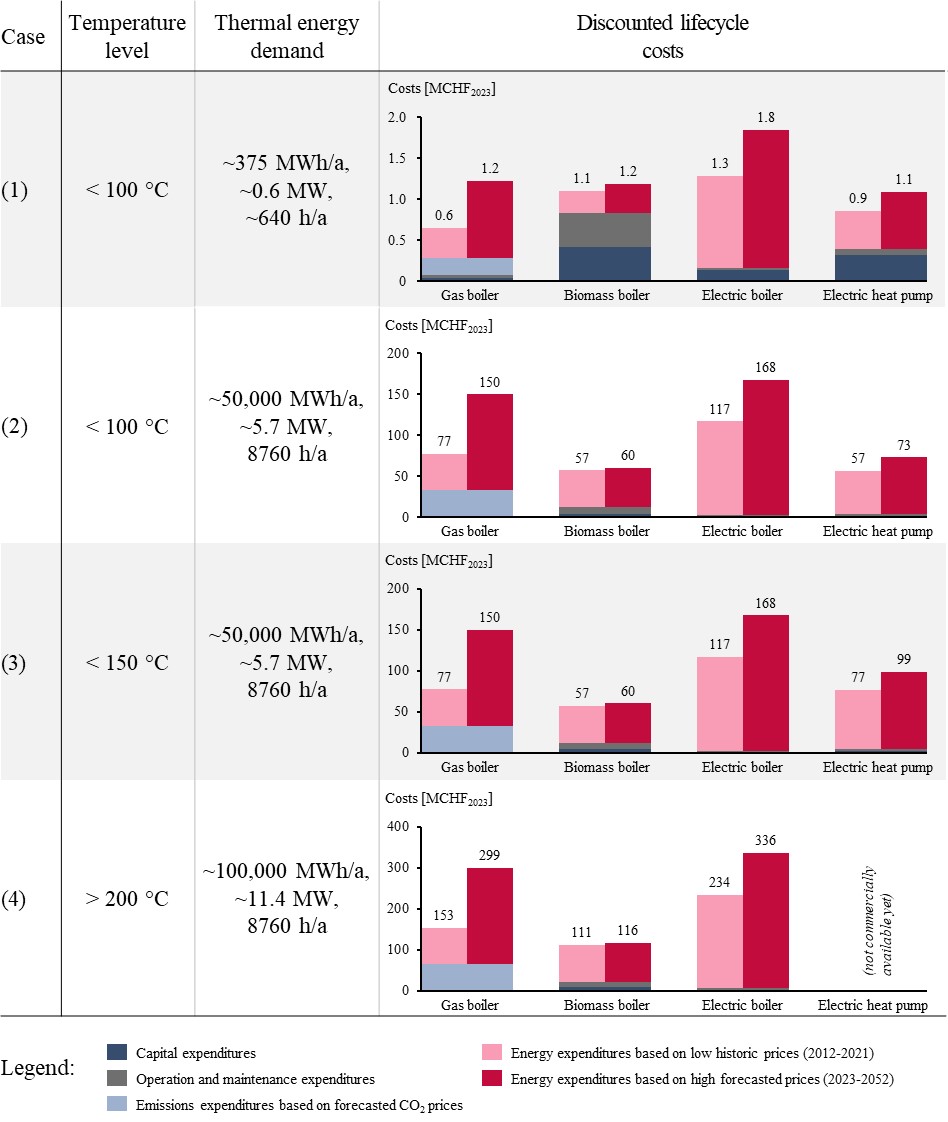

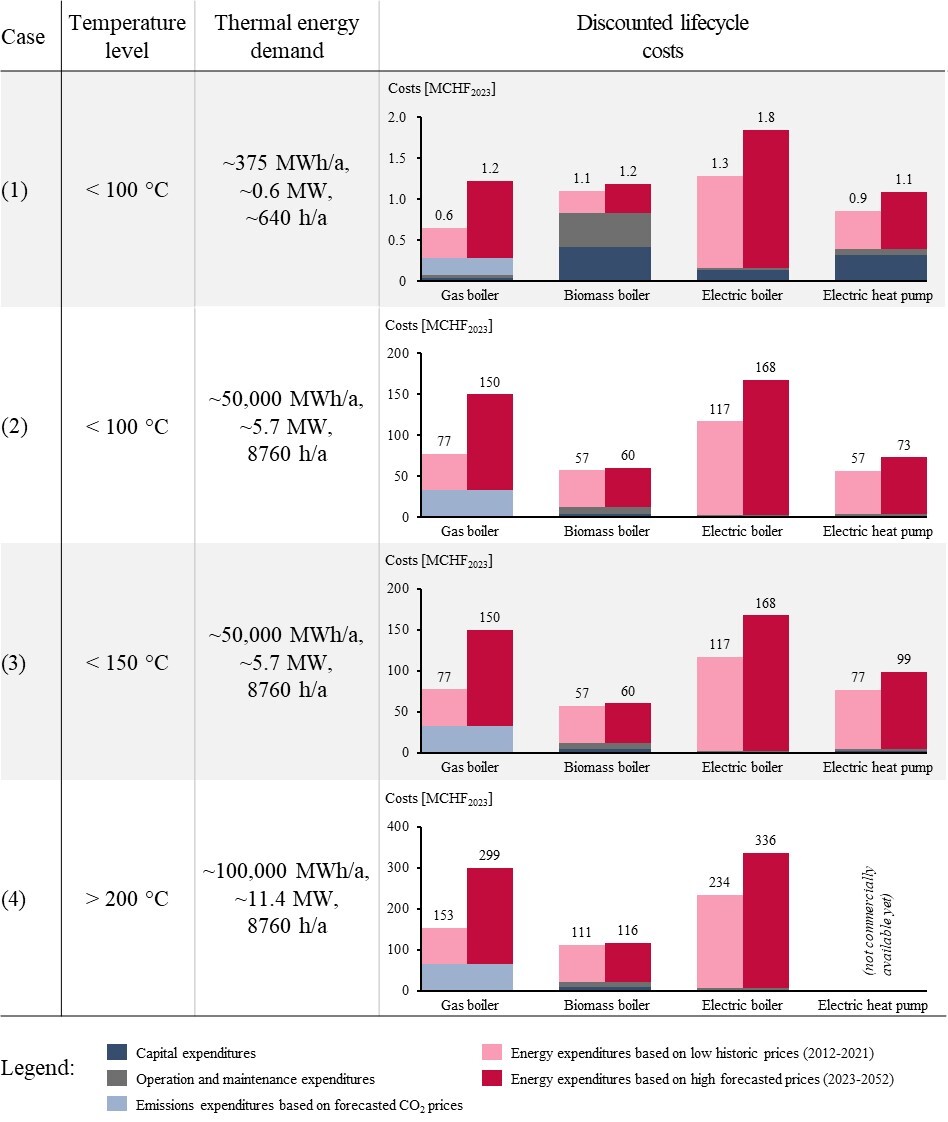

Lifecycle costs were calculated for four cases representative of the Swiss dairy industry (cf. Figure 1), each being a combination of temperature level (determined by product type) and operation size (defined by the yearly demand for thermal energy). The categorization is based on expert interviews (cf. Table 3 in the supplemental information for details on the seven interviews with dairy producers and industry experts from Switzerland) and information provided by the association of Swiss cheese manufacturers FROMARTE (2022): (1) small producers consuming ~375 MWh/a of thermal heat at temperatures below 100°C to produce products like cheese, yoghurt or butter at varying temperatures; (2) large producers consuming ~50,000 MWh/a below 100°C to produce the same products, or (3) below 150°C to produce ultra-high temperature (UHT) milk; (4) very large producers consuming ~100,000 MWh/a above 200°C to produce dairy powder.

The calculated total discounted lifecycle costs are the sum of capital expenditures (CAPEX), energy expenditures, emissions expenditures, and operation and maintenance expenditures (O&M), with yearly costs being discounted to the base year 2023 assuming a uniform discount rate (r) of 7% based on the cost of capital/internal rate of return of three relevant food processing companies in Switzerland (confidentially obtained), and summed over a thirty years lifetime (2023-2052) assuming an investment (and immediate installation) in 2023 (cf. Equation 1). In line with current policies in Switzerland (and a low CO2 footprint of the electricity mix), only gas boilers are penalized with direct emissions costs. Two different retail energy price scenarios were considered based on (1) low historic energy prices in Switzerland between 2012 and 2021 as well as (2) high forecasted energy prices. Retail energy prices are differentiated according to yearly demand, with case (1) assuming higher prices than cases (2)-(4) (EAER 2022; ElCom 2022). An inflation of 2% is assumed in line with the upper ceiling targeted by the SNB (2023).

Total discounted lifecycle coststechoper. size=years∑i=1CAPEXtechoper. sizei+ ENERGYtechoper. sizei+ EMISSIONStechoper. sizei+ O&Mtechoper. sizei(1+r)i−1

3. FINDINGS

Our findings suggest that changes in energy prices further improved the economic viability of low-carbon technologies in the Swiss dairy industry making either heat pumps (case 1) or biomass boilers (cases 2-4) the cheapest heating technology (cf. Figure 2).

For case (1), gas boilers are cheaper in the low energy price scenario, whereas for high energy prices heat pumps get most attractive, undercutting gas boilers by roughly 10%. Due to comparatively high capital expenditures and a low utilization, biomass boilers are more costly than gas boilers and heat pumps assuming low energy prices. Smaller anticipated price increases for biomass compared to gas, however, make biomass boilers slightly less costly for high energy prices.

For cases (2) and (3), biomass boilers are most economical in both energy price scenarios, followed by heat pumps. The latter are more costly for case (3) than for (2) as increasing temperatures lead to a lower coefficient of performance (COP), and consequently a higher electricity demand.

For case (4), biomass boilers are most economically viable in both energy price scenarios, followed by gas boilers. For high energy prices, electric boilers are only slightly more expensive than gas. Despite ongoing research, heat pumps are not commercially available yet for temperatures >200 °C (Liang et al. 2022).

For large producers (cases 2-4), the sum of energy and emissions expenditures contribute the largest share of total costs—more than 80% irrespective of the technology. For small producers (case 1), however, energy expenditures contribute considerably less for biomass boilers and heat pumps. Accordingly, the age of the current installations is much less important for investment considerations of large producers. Electric boilers are not competitive in any of the cases.

The presented findings hold true for changes in energy and emissions prices (cf. Figure 3): For gas boilers to become cheaper than heat pumps, electricity prices would need to increase substantially compared to forecasts for 2023-2052—ca. 100 CHF/MWh for small and >100 CHF/MWh for large producers (cf. Figure 3 A.1-A.3). Similarly, for gas to become cheaper than biomass boilers for large producers, biomass prices would need to increase by >100 CHF/MWh (cf. Figure 3 C.1-C.4). CO2 prices contribute a substantial share for low energy prices (32-41%) but a smaller share for high energy prices (17-21%). Accordingly, the findings for high energy prices are only marginally sensitive to falling CO2 prices (cf. Figure 3 D.1-D.4).

While our results show that low gas prices can no longer impede the decarbonization of the Swiss dairy industry from an economic perspective, individual non-economic hurdles exist according to the interviews conducted: biomass is not always locally available and existing electricity distribution grids cannot always handle loads associated with electrification. Space needed for biomass and hot water storages as well as larger heat exchangers are often not available in historically developed dairy plants. The reliability and maintenance requirements of biomass boilers and heat pumps are also often considered inferior to that of gas boilers—a feature particularly important when handling perishable raw materials like milk. Given the promising economics of low-carbon technologies for dairy production, however, policy and industry effort to lower these non-economic hurdles would be desirable. Overall, the prospects for a decarbonization of Swiss dairy production have clearly improved, hopefully adding another piece to the food sector decarbonization puzzle.

ACKNOWLEDGMENTS

This work was supported by the Swiss Federal Office of Energy (contract number: SI/502114-01), but the authors bear the full responsibility for the content of the article as well as the conclusions and findings presented. We thank members of EPG and CFP at ETH Zurich for their comments on earlier versions of this paper.