1. Questions

Some life-cycle cost assessments (e.g., Quarles, Kockelman, and Mohamed 2020; Krelling and Badami 2020; Holland et al. 2021) and other studies (Li, Kahn, and Nickelsburg 2015) treat buses as homogeneous except for their power types (i.e., diesel vs. electric). This study asks: How do the prices of US public transit buses vary with their attributes, such as size, floor height, etc.? The scope is limited to the United States and to single-deck, rigid transit buses.

2. Methods

We use the American Public Transportation Association’s 2024 Public Transportation Vehicle Database (PTVD) (Dickens and Bonina 2024). The PTVD is an excel file in which each row is a batch of homogeneous buses ordered by one agency in one year, with diverse information provided for each batch. To exclude errors, the data are filtered as follows:

-

Buses in active service built 2010-2023 (inclusive). This window is two years longer than the standard bus service-life in the US (Laver et al. 2007).

-

Buses listed as type transit: a rigid, single-deck vehicle with two doors, no luggage bays, at least 27.5 ft. (8.4 m) long.

-

Buses with power types (i) diesel, (ii) compressed natural gas (CNG), (iii) diesel-electric hybrid, or (iv) battery-electric. These constitute over 99% of all active buses passing (a)-(b). Buses with ‘biodiesel’ power type are treated as diesel, as the definition is ambiguous and prices are similar.

-

Buses from eight manufacturers accounting for 97% of those passing filters (a)-(c). Other busmakers seemed to have diverse errors or ambiguities. Of the eight, New Flyer, Gillig, Nova Bus, BYD and ElDorado-National are now active, while Proterra, Orion Bus Industries and North American Bus Industries are not.

-

Buses eliminated via manual checking. For example, diesel buses made by Proterra, diesel buses listed with hybrid model numbers, or rigid buses with cutaway model numbers.

-

Even after the above filtering, the dataset contained some outlier observations with suspiciously low or high prices given their year and power types. We suspected these were erroneously recorded, recorded with the wrong power type, or (in the case of low prices) purchased used. Hence, we removed observations with prices more than 1.5 IQR’s (interquartile range) from the median price for their year and power type, eliminating 2% of buses.

After filtering, the dataset contains 1,475 batches (rows) referring to 28,013 buses.

We converted the dataset’s nominal prices to 2023 USD using the CPI obtained from the priceR package in R (Condylios 2024). Next, we estimated Generalized Linear Models (GLM) to explain the real prices using a “log link” functions and a Gaussian distribution (Nelder and Wedderburn 1972; Dobson and Barnett 2018). The real price is modelled as a random variable that is normally distributed with mean where represents bus attributes and is a vector of coefficients fit to the data via maximum likelihood estimation. Estimation was weighted by the number of active buses in each of the 1,475 batches (rows) passing filters. The code for the analysis is available at https://github.com/UTEL-UIUC/bus-purchase-cost-apta.

3. Findings

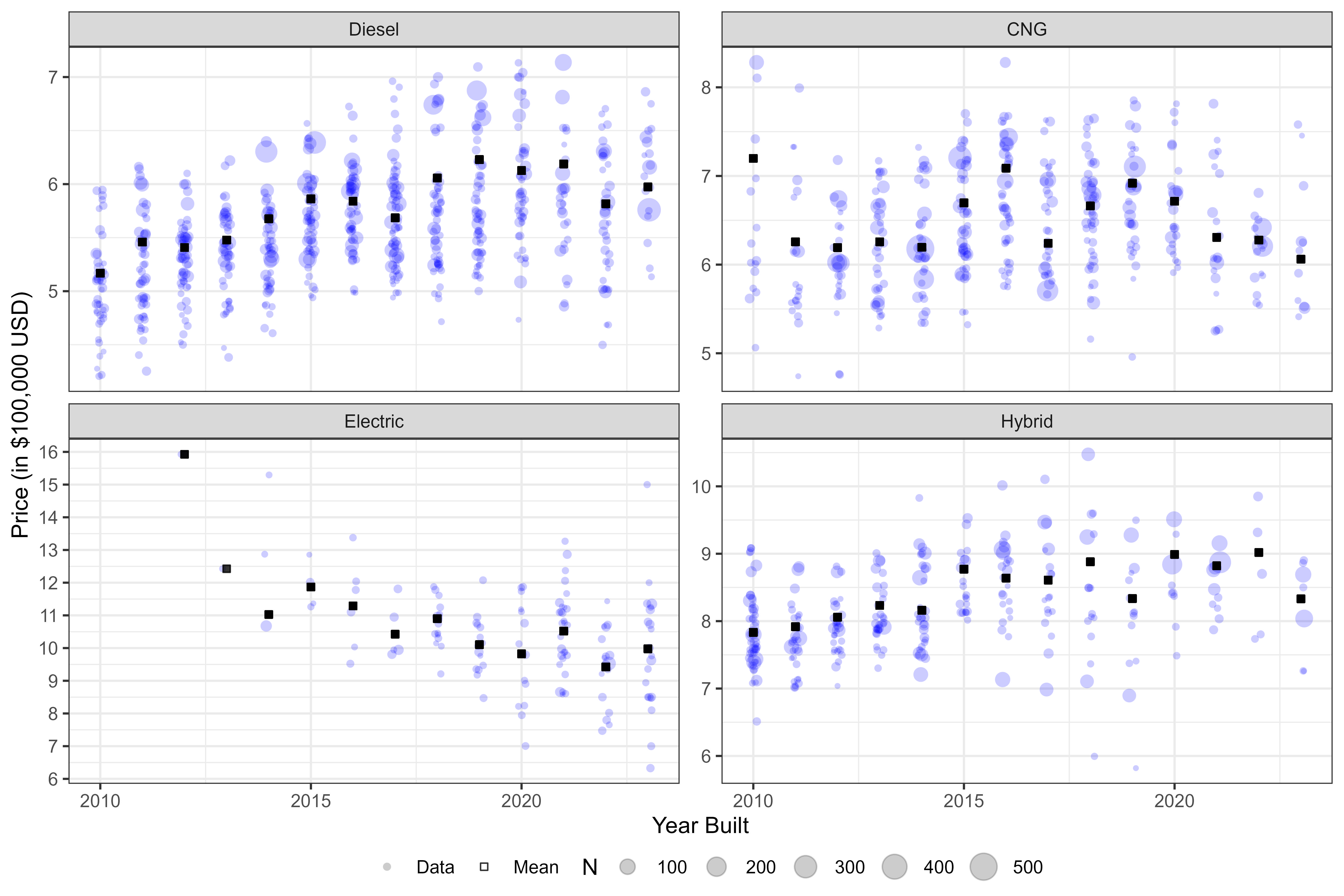

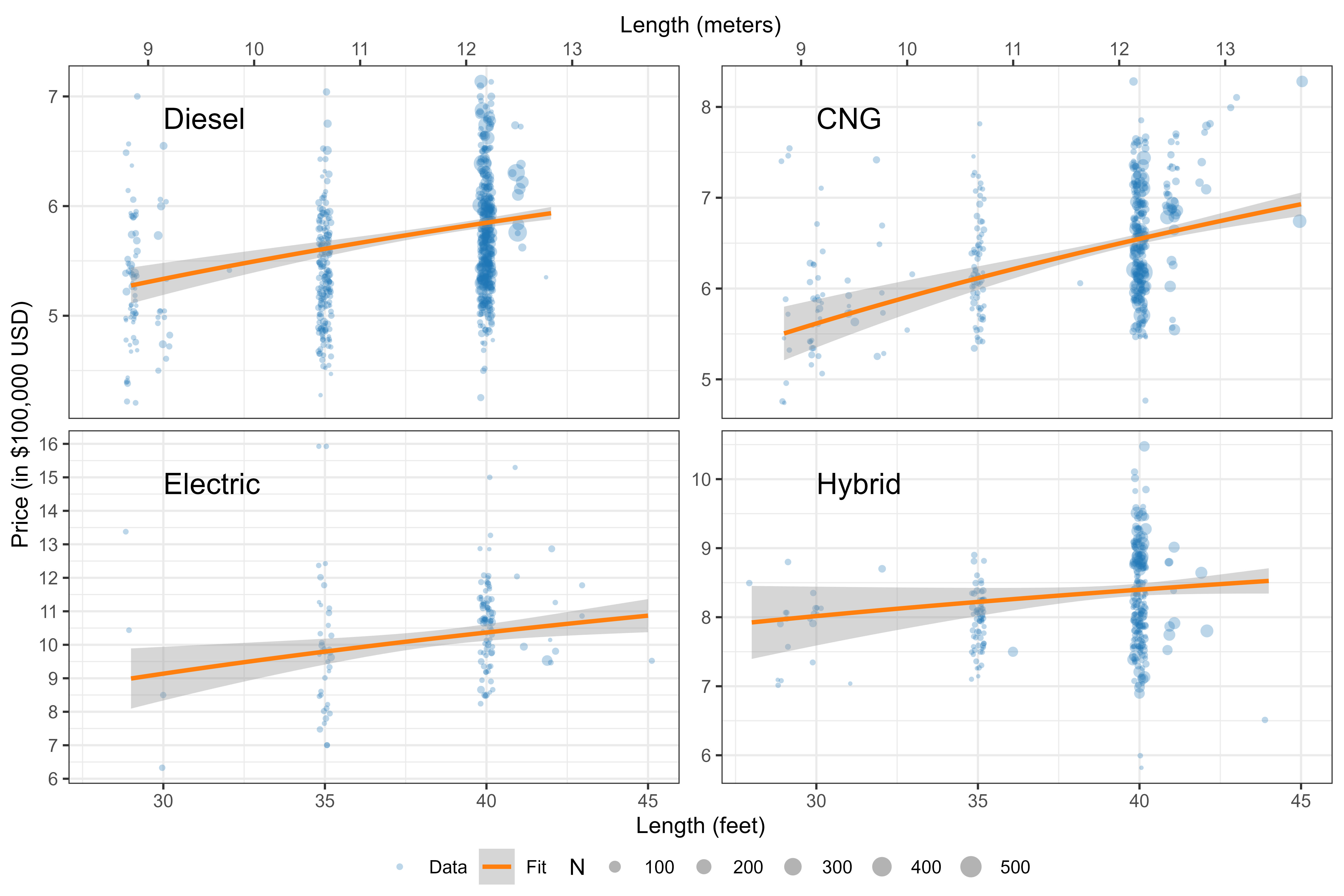

We begin with some facts about the sample. Table 1 shows the average price and count of buses by manufacturer and power type. Figure 1 shows sina (violin) plots for price, length, and seat density (the ratio of the number of seats to the product of length and width) as well as the number of buses manufactured each year. Figure 2 shows that, with the exception of electric buses, real prices (unadjusted for attributes) have generally risen over time. Figure 3 shows prices generally rise with length—albeit slowly. The sample is fairly homogeneous. Over 75% of buses are diesel or CNG, and over 75% are built by New Flyer or Gillig. 85% are 40 or 41 ft. (12.2-12.5 m) long. The dataset also includes a “floor height” indicator (low or high), although 98% of all buses are low-floor. Seat densities are around 1 seat per square yard (per 0.84 m

Table 2 reports estimation results. Model (1) covers all bus types. Its continuous variables are year, the logs of length and seat density and an interaction term “year x electric” to capture the trend apparent in Figure 2. Its discrete variables are fixed effect intercepts for high-floor body type, power types and manufacturers. The model has a relatively high (pseudo) of 0.81. Likelihood-ratio tests indicated that manufacturer fixed effects improved the model significantly, and help control for a changing mix of manufacturers over time. Model (2) was fit for electric buses as a robustness check, since electric buses appear later and have only four manufacturers. The intercept of each model is the expected price of a 40-ft (12.2 m), low-floor, New Flyer bus built in 2023 with 1 seat per square yard (0.84 m which is diesel-powered in (1).

To interpret estimated coefficients, recall the model has a log-link. The coefficient of “year” in model (1) indicates real prices of non-electric buses rose 0.7% per year, while model (2) shows real prices for electric buses falling about 3% per year. The elasticity of price with respect to length is only 0.36 in (1) and 0.29 in (2) (although the latter, smaller estimate has a larger standard error). Over the observed range of lengths (28-45 ft, or 8.5-13.7 m), these low elasticities are very close to the affine price/length relationship used in economic models such as Jara-Diaz and Gschwender (2003) and Fielbaum, Tirachini, and Alonso-Mora (2024). Surprisingly, model (1) has a significant and negative elasticity of price with respect to seat density. It seems implausible that, ceteris paribus, installing fewer seats lowers prices, but seat density may correlate with unobserved attributes (e.g., higher-quality buses intended for high-demand routes may have fewer seats) and thus should be viewed as a “control.”

For categorical variables, Table 2 reports exponentiated coefficients. CNG, hybrid, and electric buses are, respectively, about 11%, 44%, and 66% more expensive (controlling for other attributes). High-floor buses are 3.4% cheaper. The largest manufacturer effect is BYD’s 15% discount on electric buses from model (2).

Overall, the estimates suggest that ignoring variation other than power type is a reasonable, if imperfect, approximation for cost assessment or theorizing. Prices vary substantially across power types. While length has a statistically significant effect, model (1)'s price/length elasticity of 0.36 implies a 30 ft (9.1 m) bus is only 10% cheaper than a 40 ft (12.2 m) bus, when controlling for other attributes. This accords with the claim that smaller buses are not substantially cheaper (Walker 2024, Ch. 6).