1. Questions

Open-loop payments systems – those that accept credit and debit cards directly, along with digital wallets (i.e., Apple Pay) and wearable devices – are used in many industries. These systems, however, have not been adopted by many transit agencies, despite the potential agency benefits including improved passenger experience, more efficient boarding (Brakewood et al. 2020), driver safety, automated discount verification, and easier fare validation. These benefits have spurred large transit agencies including Transport for London, New York Metropolitan Transportation Authority, and the Chicago Transit Authority to implement open-loop payments.

While large agencies have resources, staff, and past investments (i.e. in Smart Card systems) that support the implementation of open-loop payments, mid-sized and smaller transit agencies may each face unique challenges in this transition (Golub et al. 2022; Perlmutter 2015). Implementing open-loop payments may require large investments in equipment and software upgrades as well as training staff to manage and use these new systems. At the same time, passengers may be reluctant or unable to adapt to digital payment systems.

Programs like the California Integrated Travel Project (Cal-ITP) aim to help transit agencies overcome challenges in implementing open-loop payments. Their programs include master service agreements that allow agencies to choose from pre-arranged contracts for equipment and payment processing and assistance with discount eligibility verification. In this study we investigate the challenges transit agencies face when considering open-loop payments and their interest in assistance programs that could help with implementation. We focus on three inter-related questions:

-

Do transit agencies want to implement open-loop payment systems?

-

What challenges do transit agencies identify when considering open-loop payments?

-

What kinds of assistance could help agencies adopt open-loop payments?

2. Methods

We collected survey data from a sample of transit agencies in California in the fall of 2022 using a combination of convenience-based and random selection. We combined a list from Cal-ITP containing 81 agencies with a random sample of the California transit agencies reporting to the National Transit Database (NTD). The initial sample included about 120 agencies (42 from the NTD and 81 from Cal-ITP). Our 21 responses yield a response rate of 17%.

The survey was informed by a small set of informational interviews, and through conversations with Cal-ITP. The survey gathered characteristics of the agencies (fleet size, modes of service, etc.), current payment and fare media, sentiments about open-loop payments, cash use among passengers, fare discounts, General Transit Feed Specification (GTFS), and interest in and awareness of Cal-ITP’s programs. The full survey instrument can be found in Turner et al. (2023). The results presented here enumerate the interest in open-loop payments and challenges faced by transit agencies considering open-loop payments. We also explore agency perceptions of support for open-loop payments among relevant stakeholders and agency interest in assistance programs.

3. Findings

Our sample includes 21 smaller transit agencies serving rural or mixed areas (Table 1). Due to the small sample size, the analysis presented here is largely descriptive. The results presented here provide insight into the potential for open-loop payments among smaller transit agencies. A few California transit agencies are piloting open-loop payments and in our sample, three agencies (14%) are in the process of implementing open-loop payments.

Table 2 presents the challenges with open-loop payments selected by 20% or more of the participants. Technology and infrastructure constraints were more frequently selected than other challenges such as contracts and internal factors, excluding staff capacity. Concerns about riders (lack of customer ability to adopt, lack of customer interest) were also selected by about one-quarter of the agencies.

Transit agencies in our study also reported their perceptions of potential barriers for passengers to transition to non-cash payments. Though cash may be accepted alongside open-loop payments, agencies often reduce costs by discontinuing cash payments when adopting open-loop systems. Passengers without bank accounts or who are reliant on cash for daily financial activity may be less able to adapt to open-loop payments. Our agencies perceive the top passenger challenges in adapting to non-cash systems to be new technology and banking.

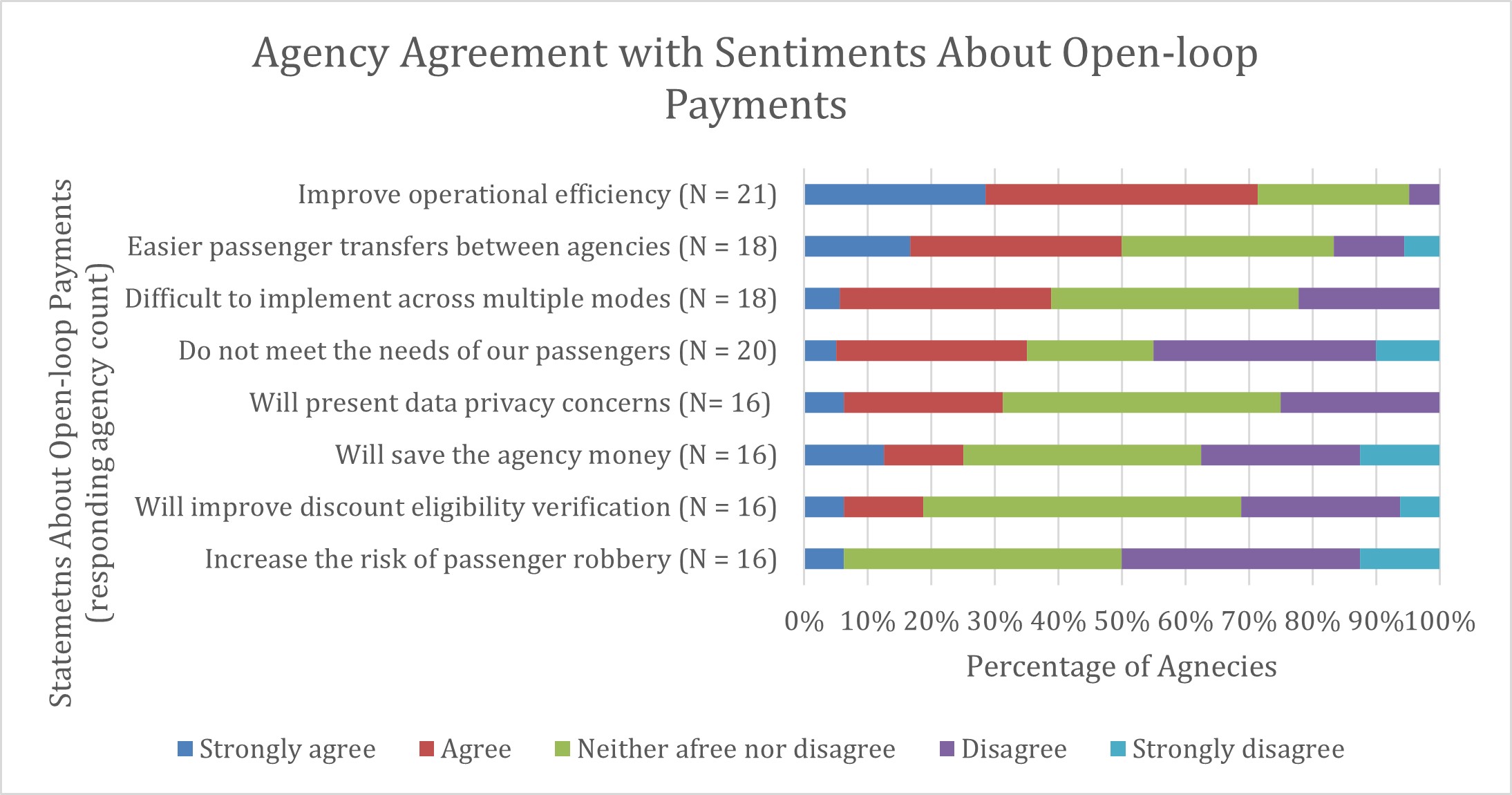

Our respondents also had positive sentiments about open-loop payments more generally (Figure 1). The majority (71%) agree or strongly agree that open-loop payments will improve operational efficiency, while approximately half agree that they will make inter-agency transfers easier for passengers. Positive sentiments are also reflected in disagreement with “increase the risk of passenger robbery”. Agencies were split on “do not meet the needs of passengers,” and were more neutral about discount eligibility verification and data or privacy concerns. Finally, they had somewhat negative perspectives on financial savings.

__1_2_.jpg)

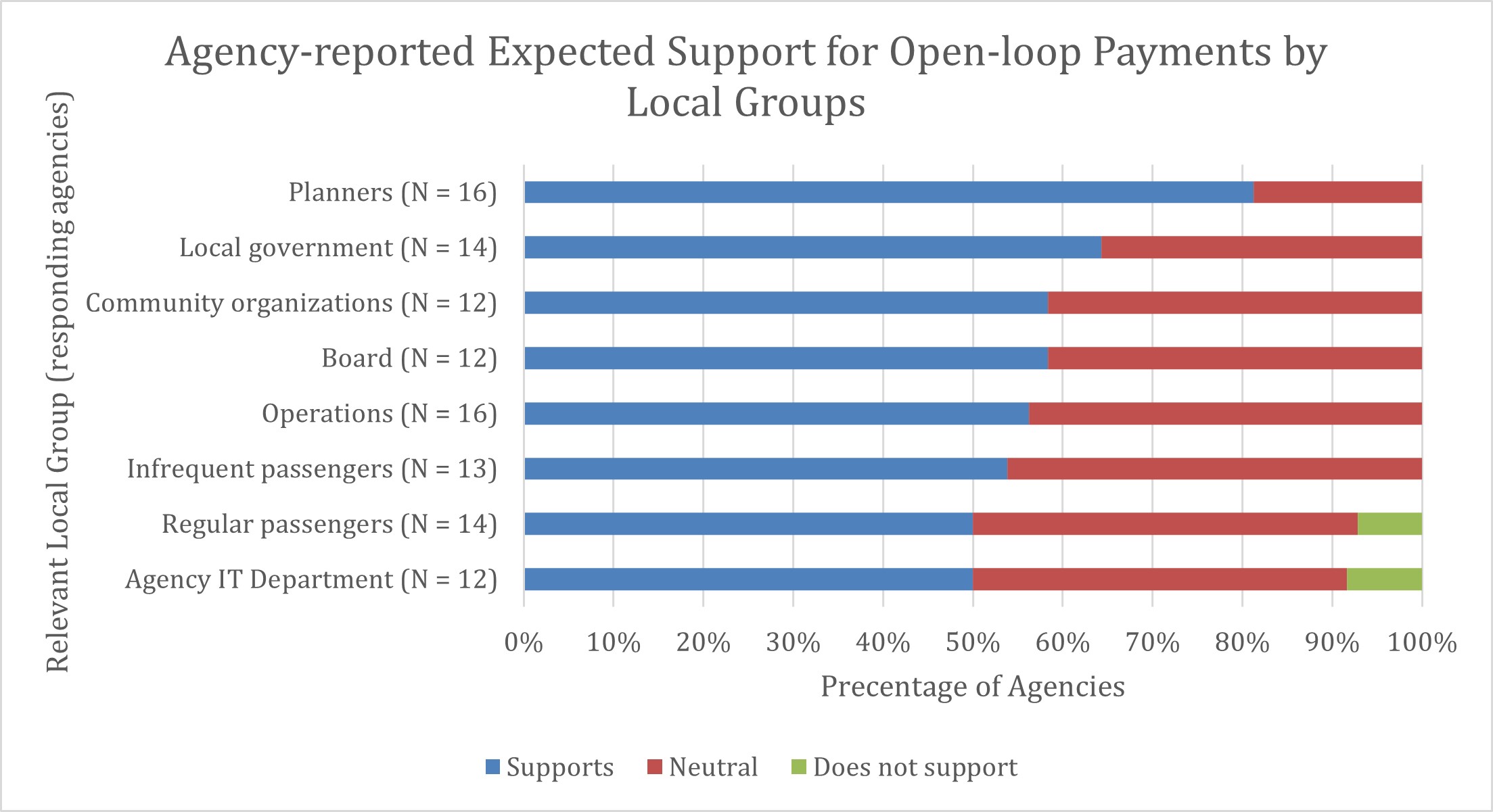

We also asked the agencies their perspectives on the support for open-loop payments among those associated with the agency (Figure 2). At least 50% of those responding to each question perceive the relevant group as supporting or strongly supporting open-loop payments, while the remainder are neutral.

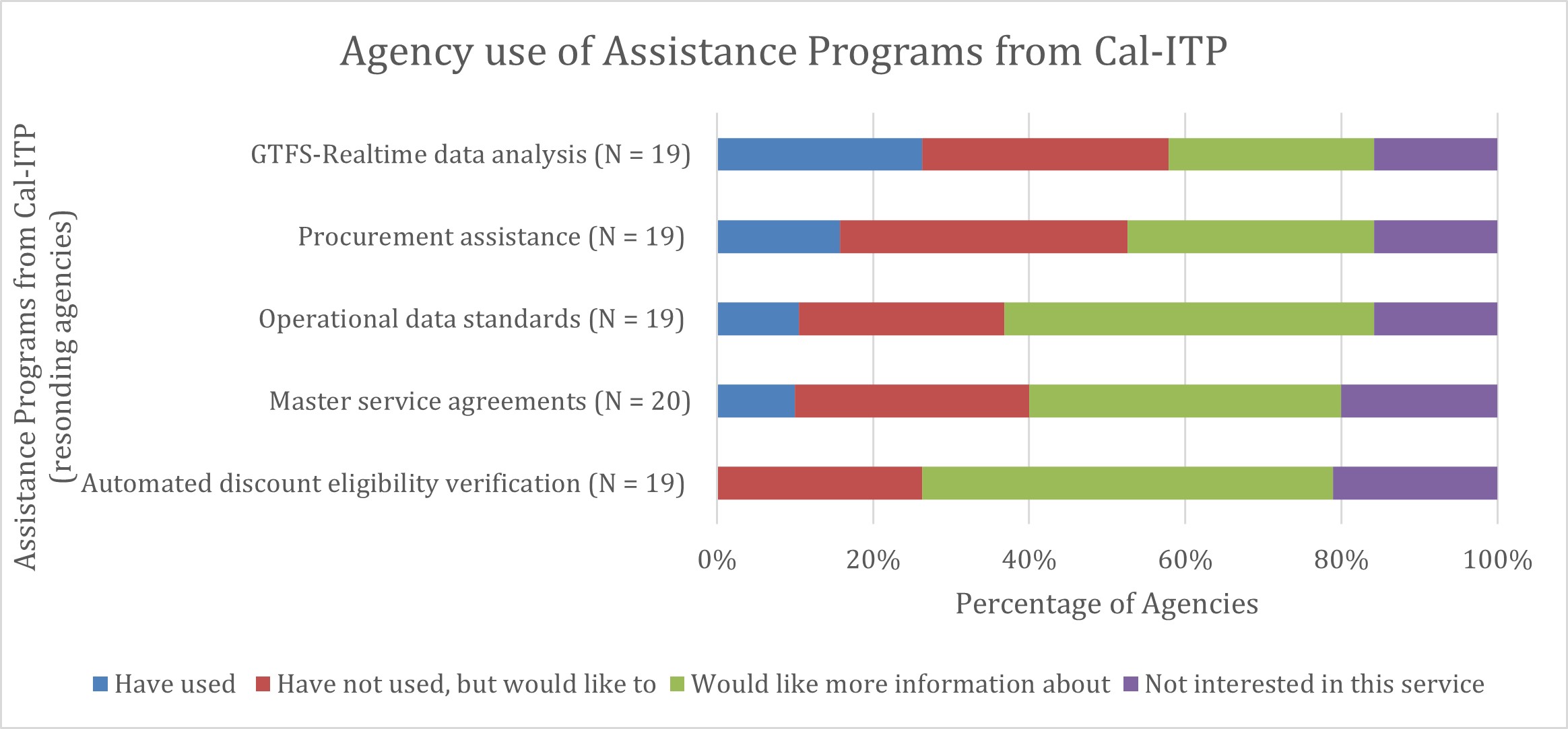

To address the challenges associated with open-loop payments, Cal-ITP offers transit agencies assistance. Though some agencies participating in our study are not familiar with all of the Cal-ITP programs (see Turner et al. 2023), we find that they want to learn more about or use many of them (red and green segments in Figure 3). A few agencies have used some of the programs, while at most 21% of the sample is “not interested” in each program.

_1_.jpg)

Our results show that agencies are interested in open-loop payments, but that they do face challenges with implementing these new systems. There is, however, a high level of interest in assistance programs among the small and mid-sized agencies in our sample. This suggests that these kinds of programs may provide a means for small and mid-sized agencies to overcome challenges due to the lack of staff, financial, or other resources when considering open-loop payments. State level programs such as those offered by Cal-ITP can create economies of scale, facilitate the exchange of knowledge, provide a model for contract terms and vendor agreements, and improve outcomes for passengers. These assistance programs may serve as a template for similar assistance programs and policies in other areas of the US and some elements may even translate internationally.